|

|

RECENT POSTS

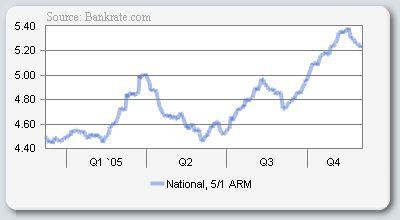

Wednesday, December 28, 20050 Comments Tuesday, December 27, 2005Timing DilemmaI need to write this out only because I have a timing problem that I'm dealing with. Here is the situation: 1. I have a $75,000 loan that needs to be paid within 5 years, which is more than conservative. 2. I need to finish college which will be a year and a half to two of those 5 years. Then I will be at my dream job doing what I always wanted to be doing in the first place. 3. We need to concieve a child in the 5 year time frame and time it, so that I will be able to watch the child at home during my college days. That way both myself and my spouse will have time to interact with our child. 4. I need to save enough money in my emergency fund to cover expenses while living off one salary, one set of benefits for our family for 1-2 years. 5. Because my existing student loans will be deferred whilst in college, I dont have to worry about paying back the expense right now. However, I do need to know if I should be accumulating more student loans to pay back later or to save enough and risk our emergency fund on ~$12,000 tuition at the university? This would equal with my current loan of ~$5,500 to $17,000... plus my spouses existing student loan of $16,000 which will bring it to $33,000. 6. We need to purchase a new home in 5-7 years because our family will be growing. Our current home equity is at $50,000 but I wouldn't doubt that it would sell higher. 7. We need to fix up the house that we are currently in. We have updated the kitchen and are currently working on a budget to fix our fence and add new insulation to the attic. 8. My job is currently very unstable and I wish not to participate in it forever. My youth is slipping away at 25 and I need to get on my track to enjoy my working days. After that, I will be content to work for approximately 25-30 years depending on savings ect. 9. Savings, 401k and Roth IRAs will have to still have contributions b/c I cant neglect this but with a one person salary it may be difficult. Im thinking while going to full time school and watching our newborn, that i will have time to have a small part time job??? 10. My time frame is 5 years, 6 years Max. What to do? :/1 Comments Thursday, December 22, 2005Mortgage payoffReviewing my option to pay off my mortgage earlier. Within the 5 year limit seeing as I have a 5/1 ARM and know what happens to the interest rates afterward. Im thinking that even with my money now going to ING, I'm surprised that I could have done more with my previous mortgage company. I didnt put in any extra payments towards them and at the refinance was the only time that I paid into the loan, basically to bring it down to $75,000. My life is going to revolve around these next 5 years approaching and I'm considering leaving my job.My spouse would be the sole breadwinner in the home with a take home income of approximately $2100 a month after taxes. This is not including any kinds of insurance that we may have to get. I was running numbers to figure what type of fund I should have before I venture off without a job. I was even thinking that a measly part time job would be worth it because we could use the money from my paycheck to sustain us for food and fun however the bills would be taken through her monthly allowance. More accurate numbers on this later... TBC 3 Comments Wednesday, December 14, 2005PF sitesCurrently I'm looking at a few interesting sites.http://www.networthiq.com and http://www.everybodylovesyourmoney.com These are great PF sites that I would recommend for a good read! 0 Comments Sunday, December 11, 2005Retire EarlyWith all the reasons why NOT to retire, there are always bright sides.Top 10 Reasons to Retire Early Reason number 10. I want to spend more time with my family. Reason number 9. I want to spend more time huntin' and fishin'. Reason number 8. I want to lower my golf handicap. Reason number 7. Work interferes with what I really want to do with my life. Reason number 6. I'm not interested in working nights and weekends. Reason number 5. Once I'm retired, every day will feel like Saturday. (Of course, we hope this doesn't apply to those currently working nights and weekends.) Reason number 4. In this company, looking busy means more than being productive. (Especially, looking busy on nights and weekends.) Reason number 3. It's the ultimate in employee empowerment. Reason number 2. Instead of contributing to my 401k, I should be shorting company stock. And, the number 1 reason to Retire Early. I'm sick of kissing the great white corporate behind. courtesy of: http://www.retireearlyhomepage.com Copyright © 1997 John P. Greaney 0 Comments Emergency FundingWe are enjoying our new found freedom due to the refinance and dumping most of our savings into paying down the mortgage for the refinance. Our current mortgage equals $82,658. New Mortgage on the refinance paid down to $75,000 even. We have trashed our $13,500 savings and put $7,000+ towards paying the refinance and the remaining $5,000 we are using as our own personal savings. Now a couple days ago, I was in a quandary in which I had $5,000 cash in my hand after taking out of the checking account. I placed it in an envelope and stuck it in a safe place (not earning interest). I have made an "emergency fund".The Emergency Fund. I plan on not touching the fund and thought, well if I'm not going to touch it but I want its liquidity, I might as well take it as cash. Then I thought wouldn't it be better if I put it in a money market account with checking priviledges?? I mean it might as well be safer than sticking it in a safe place, right? Well thats the point where I am in the emergency fund. The spouse wouldn't mind the emergency fund being bigger. I think 6 months worth of expenses, which means approximately $10,000 should be enough. Im guessing thats the amount that would make me feel safer too. Emergency funds are meant to be SAFE and LIQUID. Period. From a personal standpoint, I'll never be satisfied with an emergency fund because I'll never feel comfortable with a certain amount..... As I'm writing this I'm deciding to do an exercise. Monthly expenses are as such (minus IRAs and Savings contributions): - $975.00 total. Approximately $1000. So if we were to both lose our jobs, $6,000 should be enough. At the worst we can always throw ourselves into the depths of hades, ie: credit cards, 2nd mortgage. I say when we are at our worst moments, I DO NOT want to have to dig deep or put any more money into debt. Why? Because deep down it scares me to have to lose the house or to find my family living on the street somewhere. $6,000 doesnt cut it in real life. I have to figure that $20,000 should be enough AFTER all debt has been paid (monthly at that time will drop down to $500). The emergency fund should sustain for more than 2 years with a family. Our next worry... purchasing our 2nd home. 3 Comments Thursday, December 01, 2005Refi source Looking at the 5/1 ARM chart, we are on the tail end of the 4th quarter showing a dip in national rates for this type of mortgage. (chart provided by http://www.bankrate.com) 0 Comments The First Time RefinanceIts time to refinance the mortgage. Now the first mortgage that we have through Homecomings Financial did not work out because the 3/1 ARM option they picked was garbage and will expire soon to a hideous 9.99% interest rate (Are they crazy??? My Credit Cards get better rates!). I always find that I choose the wrong financial option the first time around and then the second time I realize how dumb my first choice was. The second option suits me much better in our financial position. We refinanced through ING Direct and started the ball rolling yesterday.As excited as I was refinancing, I can't wait til the day of closing. Here were the couple of snags I ran into. First, they wanted to know if my spouse and I wanted to be on the same title. Since the original title is solely in my name and it would cost an extra $200+ to get this done, I decided not to add the spouse onto the account. The ONLY reason why you would make this a joint account FINANCIALLY speaking, is if you wanted the debt:income ratio to be much lower since 2 incomes are better than one. I decided NOT to have the spouse on the account since we technically will own the house in 3 years or less anyway; the title AT THAT TIME after it is free and clear, can be changed into whatever I wish. The closing costs were minimal and shouldnt be more than $1000. The interest rate that I closed last night has since dropped a couple hundredths of a percentage point making our monthly rate drop $10/month!! How incredible is that? Here is our setup: $75,000 Mortgage Loan on a $125,000 house. Interest rate locked in at 5.625% for 5 years. Monthly payment calculated at $432.00/monthly Additionaly monthly payment to principal: $1668.00 (total payment will be $2100/month) Using this, my loan will be fully paid off in 3 years. I accepted this and have been submitting paperwork to ING mortgage as quickly as possible. However.... this NEW loan has brought up some interesting questions. Since I will ultimately be draining my savings account now at $13,500.00 (putting 7,500 towards paying off my loan of $82,000 on my first loan) , how will I use the remaining $6,000.00?? My first idea is to build an emergency fund of $6,000, however I don't want to use the full amount. I believe that 6 months worth is more than enough for us. I will start the emergency fund with $2,000. The remaining balance we will use towards renovations on the home. NOW the kicker.... since my loan is for approximately 3 years ending sometime in 2008, when my spouse is 27 and I'm 28, when will we have children? And on the side of education, when will I have time to finish my bachlor's degree? I have been running numbers all day and have come to the conclusion that I will run my current job into the ground, while attending night classes to finish school. Then during my senior year in 2008, I will have graduated and moved onto my dream job. Somewhere in there, I need to balance school, a very very unstable job, my spouse, and possibly unexpected children (which if do happen, we are more than prepared). These are a few insights as to what comes with a mortgage like this. I can't wait for the day when we don't have to worry about a mortgage over our head or have any debt! 3 Comments |